Supplementing the Gaps in Your Original Medicare Coverage

Along with Original Medicare, many people consider additional coverage for the co-insurance, co-payments, and deductibles not covered by Original Medicare. This coverage is known as Medicare Supplement Insurance, often referred to as Medigap coverage.

Original Medicare is a great start for your retirement health insurance. However, it was not designed to be comprehensive coverage and out-of-pocket expenses can start adding up. Those gaps in coverage, representing a financial burden to retirees, led Congress to authorize the creation of “Medigap” insurance, also known as Medicare Supplements, which control the potential out-of-pocket expenses contained with Original Medicare.

Medigap is not a replacement for Original Medicare. You still need Parts A and B and must continue paying any monthly premiums that come with those. You will pay a private insurance company a separate premium for your Medigap Insurance.

Medigap Eligibility

When you turn 65, and are enrolled in Medicare Part B, you have a guaranteed issue period. During this time, you can buy any Medigap or Medicare Supplement policy sold in your state without being subject to medical underwriting. Regardless of any pre-existing medical conditions, you will be able to buy the same policy at the same price as someone in perfect health.

However, if you choose not to buy a Medigap policy during your guaranteed issue period, and decide later that you need the additional coverage, you may not have the same options (depending on your state of residence). After your Medigap guaranteed issue period ends, you could be subject to medical underwriting, and potentially can be denied enrollment in a Medigap plan (again, depending on state of residence). Consider purchasing a Medigap policy during your guaranteed issue period to reduce your long-term costs and ensure that an insurance carrier will sell you a Medigap policy.

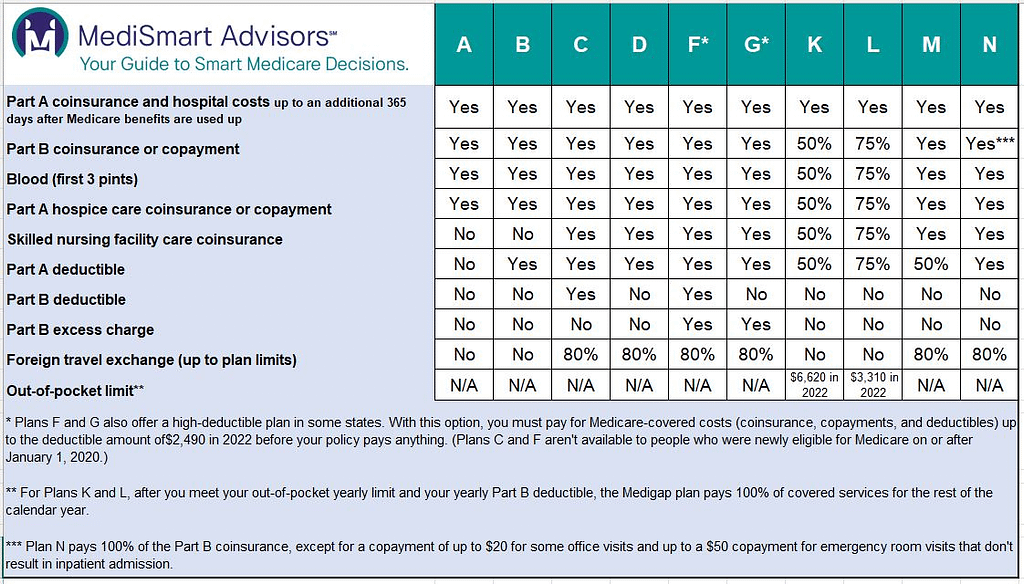

Choices in Medicare Supplemental Insurance

Medigap plans are standardized. What that means is that all plans of the same letter are identical, regardless of the Insurance carrier that issues them. The only difference is the price, as each issuer may set their own premium. Medigap plans are identified by letters: A, B, C, D, F, G, K, L, M, and N. Some plans are no longer sold, but those who already have them are grandfathered.

(It’s important to note that Medigap policies in Massachusetts, Wisconsin, and Minnesota are standardized differently.)

Finally, Medigap insurance stands in your place in being the payer of bills that would otherwise come to you. Important to note that supplement plans are required to cover all Medicare-approved procedures that the plan type covers, but does not cover long-term care, vision and dental care, eyeglasses, hearing aids, or any other expense not covered by Medicare, with a few limited exceptions, such as International Emergency coverage.

Identifying the coverage gaps in Original Medicare and knowing which plans offer the best value for your medical needs gets complicated and it is something you cannot afford to get wrong.

Speak with MediSmart Advisors to better understand your options.